The housing market in Canada, and particularly Vancouver and Toronto, is in a bubble. Though some people still pretend that isn’t the case, any reasonable examination of the Vancouver market will reach that conclusion. For instance, real estate is typically considered affordable at a price to median income ratio of 3, and considered severely unaffordable at a ratio of 5. Vancouver’s ratio is somewhere in the 11-13 range, and pretty well every other valuation metric is similarly skewed.

Borrowing binge

The primary cause of this bubble has been low interest rates combined with CMHC insurance. The low interest rates make consumers willing to take on massive amounts of debt because the short-term monthly payments are manageable. The CMHC insurance makes banks willing to give them money by eliminating the risk of a loss.

This might seem nuts considering real estate valuation ratios, but it is the right strategy for both players, because for both, it’s a “heads I win, tails someone else loses” scenario. Low-net worth consumers should leverage themselves up as much as possible. If houses keep going up, they get rich, while if they fall, they can just default. Same for the banks. If the borrower doesn’t default, the bank make money. If they do default, the CMHC will take the loss. Strategically, these asymmetric bets are a great deal.

Meanwhile, the Canadian government that originally kicked off this binge by allowing 40-year amortization mortgages and encouraging borrowing with the home renovation tax credit has started to see the errors in its ways. Though it claims there is no bubble, it has taken several actions to try to cool the market down, such as dialing back the 40-year mortgages, forcing short term borrowers to use 5-year mortgage interest rates in the calculation to determine mortgage eligibility, and scolding Canadians for taking on too much debt.

It’s good to be drunk

The reason the government is concerned is because of the long term impact of the bubble on the economy. Over the short and medium term, a speculative bubble is great. So many people benefit from houses being built, updated, and flipped–real estate agents, bankers, lawyers, contractors, hardware store employees…. The list goes on and on. The incentives are aligned so almost everyone in the business of real estate benefits directly from a bubble.

Then there are the secondary effects, neatly summarized by the Premier of British Columbia Christy Clarke. People can use “the equity in their home to maybe get a loan or use that to finance some other projects.” In essence, she saying that homeowners can borrow against bubble-inflated asset values and use the money to stimulate the economy.

I see people doing this, taking loans against their house to buy vacations or big-screen TVs that they otherwise couldn’t afford. When I gently inquire about their reasoning, they typically say that their house has gone up in value by more than the new debt they’ve taking against it.

The problem of hangovers

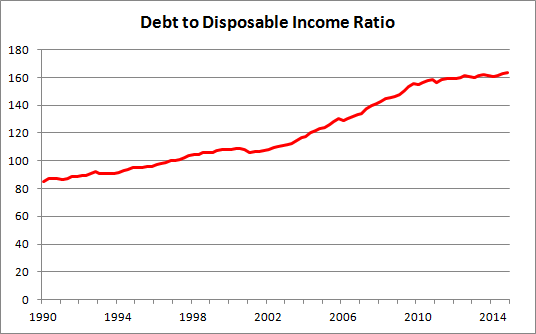

The problem with this strategy is that debt cannot grow indefinitely. In the 1990s, Canadian debt to disposable income levels were under 90%. Today, they’re over 160%, above the levels in the USA when their housing bubble popped.

Savings rates in Canada are at record lows. British Columbians have had a negative savings rate for years. If they simply begin to spend only what they make, it will have a major negative impact on the economy. If they actually try to save again (or really, actually start paying off their debt), then it will be even worse. It will cause a recession or a depression.

The long term impact will likely be severe for many people, because a house isn’t a retirement plan. A large subset of Generation X is dumping all its income into bricks and won’t have the liquid assets needed to retire. When the leveraged bet on overpriced real estate fails, many will be wiped out and unable to recover.

Recently, there has been talk about the hollowing-out of the middle-class. Well, the middle-class in Canada is doing it to themselves by buying overpriced land.

The way out

The problem now is that there are really no good options to avoid the consequences of this bubble—it’s been going on too long and become too large for there not to be major casualties when it pops. So now, the Bank of Canada is starting to examine a new option to minimize the pain of a housing crash. I like to call their proposed solution, “reward speculation, punish prudence”.

“because a house isn’t a retirement plan.”. But it is for many as it offers, a home to raise a family, status within the community, an illusion of stability. If one accepts the premise then one decision; buy a house, means one does not have to worry about icky things like investment portfolios etc. Many folk cannot cope with more that one egg in the basket!

LikeLike

Yes, I think that’s the psychology behind it. The problem is that the math doesn’t work that way. (i.e. I think it’s likely that in 25 years, there will be a bunch of seniors who can’t retire because they spent all their income on a house and didn’t save anything.)

LikeLike